With the SEC’s disclosure proposal comment period recently ending and likely climate-related disclosure regulation coming soon, it is imperative that companies begin to not only understand how to compile this information, but also work quickly to stand up ESG programs. Not only is it important to establish an ESG framework and set goals for progress accordingly, it’s critical that organizations are held accountable for those commitments. Part of the SEC proposal states that if an organization has set a net-zero target, they will need to demonstrate how this will be achieved – this includes actions like carbon offsetting and renewable energy certificates.

The calculation of GHG emissions causes confusion for many organizations, especially those just getting started with their ESG programs. This article is dedicated to explaining Scopes 1, 2 and 3 – and what organizations need to know to prepare for disclosure regulations.

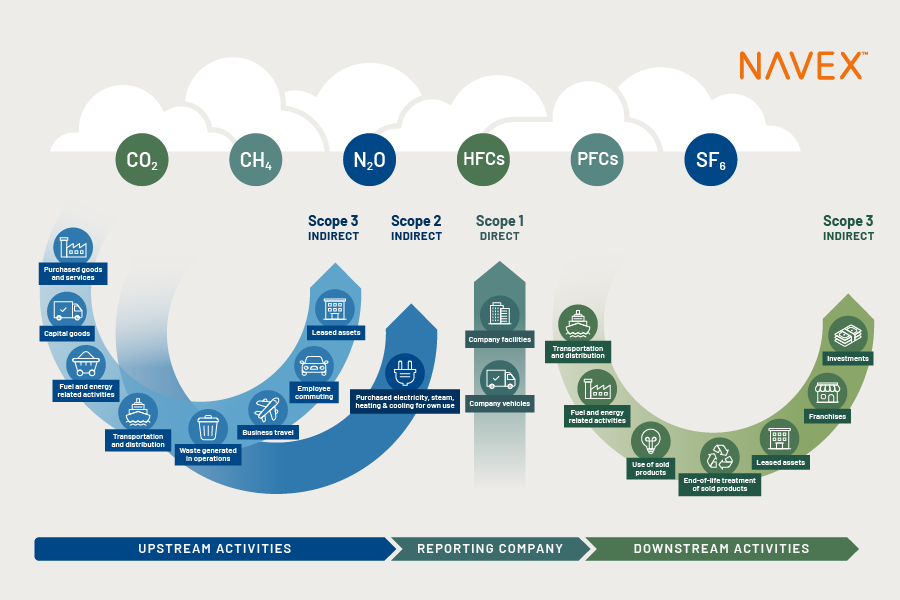

First, Direct and Indirect Emissions Explained

Before we dive into the Scopes, it is important to discuss the difference between direct and indirect emissions. The GHG Protocol defines them as follows:

Direct emissions are emissions from sources that are owned or controlled by the reporting company.

Indirect emissions are emissions that are a consequence of the activities of the reporting company, but occur at sources owned or controlled by another company.

Next, Scopes 1 and 2

Scope 1 is the most easily understood of the three as it encompasses direct emissions. Scope 2 and 3 include indirect emissions, which the reporting company doesn’t control, but can influence.

As outlined by the GHG protocol, examples of Scope 1 emissions include:

- Emissions from combustion in owned or controlled boilers and furnaces

- Reporting company owned vehicles

- Emissions from chemical production in owned or controlled process equipment

Scope 2 emission examples commonly include the use of purchased electricity, steam, heating, or cooling.

Finally, What Exactly is Scope 3?

Because Scope 3 emissions are the most difficult to calculate and define the scope of, we’ll address this separately.

The simplest explanation is, Scope 3 encompasses everything outside of what Scope 1 and 2 cover. The scopes are mutually exclusive for the reporting company in order to avoid double counting of emissions. Put another way, Scope 3 emissions calculations do not include those already accounted for in Scopes 1 and 2. Because of this delineation, Scopes 1, 2 and 3 make up the total GHG emissions related to a given company’s emissions.

The GHG Protocol provides further clarification as follows:

“By definition, Scope 3 emissions occur from sources owned or controlled by other entities in the value chain (e.g., materials suppliers, third-party logistics providers, waste management suppliers, travel suppliers, lessees and lessors, franchisees, retailers, employees, and customers).”

This infographic further explains the differentiation between Scopes 1, 2 and 3:

Emissions Disclosure – What Your Organization Needs to Know

There are many elements to the SEC disclosure proposal and the full fact sheet can be found here. But perhaps the most actionable piece of the proposal is how companies will execute GHG accounting.

Scope 1 and 2 emissions will need to be accounted for, (for some) independently attested to and validated, and then disclosed. Scope 3 disclosure will have a longer phase-in period and smaller companies will be exempt from this disclosure.

As stated by the proposal, “Indirect emissions from upstream and downstream activities in a registrant’s value chain (Scope 3), if material, or if the registrant has set a GHG emissions target or goal that includes Scope 3 emissions…”

“If material” is doing a lot of work here- and is most relevant if identified as a part of a company’s materiality assessment – a key element of formalizing an ESG program. Scope 3 calculation is difficult to account for since it is the largest and most complex aspect of emissions. If passed as is, there will be a phase-in period for disclosure of Scope 1 and 2 and an additional phase-in period for Scope 3. In addition to the longer phase-in period and exemption for smaller reporting companies, there will also be a “safe harbor for liability” for Scope 3 disclosure.

It's worth noting that this proposal does try to walk a fine line between business concerns around measuring Scope 3 emissions while holding organizations as accountable as possible for their climate related disclosures. Additionally, “smaller reporting companies” will see softened requirements for Scope 3 disclosure.

For now, organizations should start calculating Scope 1 and 2 emissions and if they haven’t done so already, start allocating resources to build a scalable ESG program. This includes dedicated personnel and systems, such as a software solution, to compile the metrics and prepare for disclosure. While not all organizations will be required to disclose their progress in ESG, it is quickly becoming an expectation of investors and consumers alike.

For more resources on how to develop a scalable ESG program, download